The interdependence between economic growth and financial stability requires (amongst other things) sound performance and management within the banking sector. This interdependence extends to general, life and health insurers and RSE licensees, as collectively with ADIs, they are the core institutions within the Australian financial system.

Consumer trust and business sentiment may also affect the utilisation and investment within the financial system. A loss of trust, confidence and investment in financial entities may also have a negative effect on economic growth. It is for these reasons the Government had introduced the BEAR legislation “to improve the operating culture of ADIs and increase transparency and accountability across the banking sector…enhancing the obligations of ADIs and reinforcing the standards of conduct expected of them by the community”[i]. The Financial Accountability Regime (FAR) builds on this by increasing the obligations and expanding applicable entities beyond ADIs. FAR commenced for ADIs on 15 March 2024 (although the transition period for compliance has been extended by ASIC and APRA to 30 June 2024). FAR will commence for insurers and RSE licensees on 15 March 2025. Entities captured by the FAR obligations are called ‘Accountable Entities’[ii]. Entities that are ‘Foreign Accountable Entities’ are subject to similar but not identical requirements, and we will discuss those in a separate article.

Lines of Business

FAR enhances the responsibilities of Accountable Entities and draws a notional line of responsibility for a ‘line of business’. The FAR obligations make key personnel accountable for the performance of their respective ‘line of business’ from a managerial and operational perspective. Personnel with senior executive responsibility for the below functions in the business are Accountable Persons[iii]:

- Financial Resources

- Operations

- Risk Controls or Risk Management

- Compliance

- Information Management

- Internal Audit

- Human Resources

- Dispute Resolution

- Breach Reporting

- Client Remediation

- Anti-Money Laundering

Accountable Persons are Obliged to:

“take reasonable steps in conducting the responsibilities of their position” …to prevent matters from arising that would likely arise and adversely affect the prudential standing/reputation of the Accountable Entity and to prevent material contraventions (of relevant laws)”. [iv]

Implementing measures and ensuring their business are functioning in a sufficiently transparent manner so that the Accountable Person has visibility of the business operations and compliance of the Accountable Entity and any potential effect on consumer trust and business expectations.

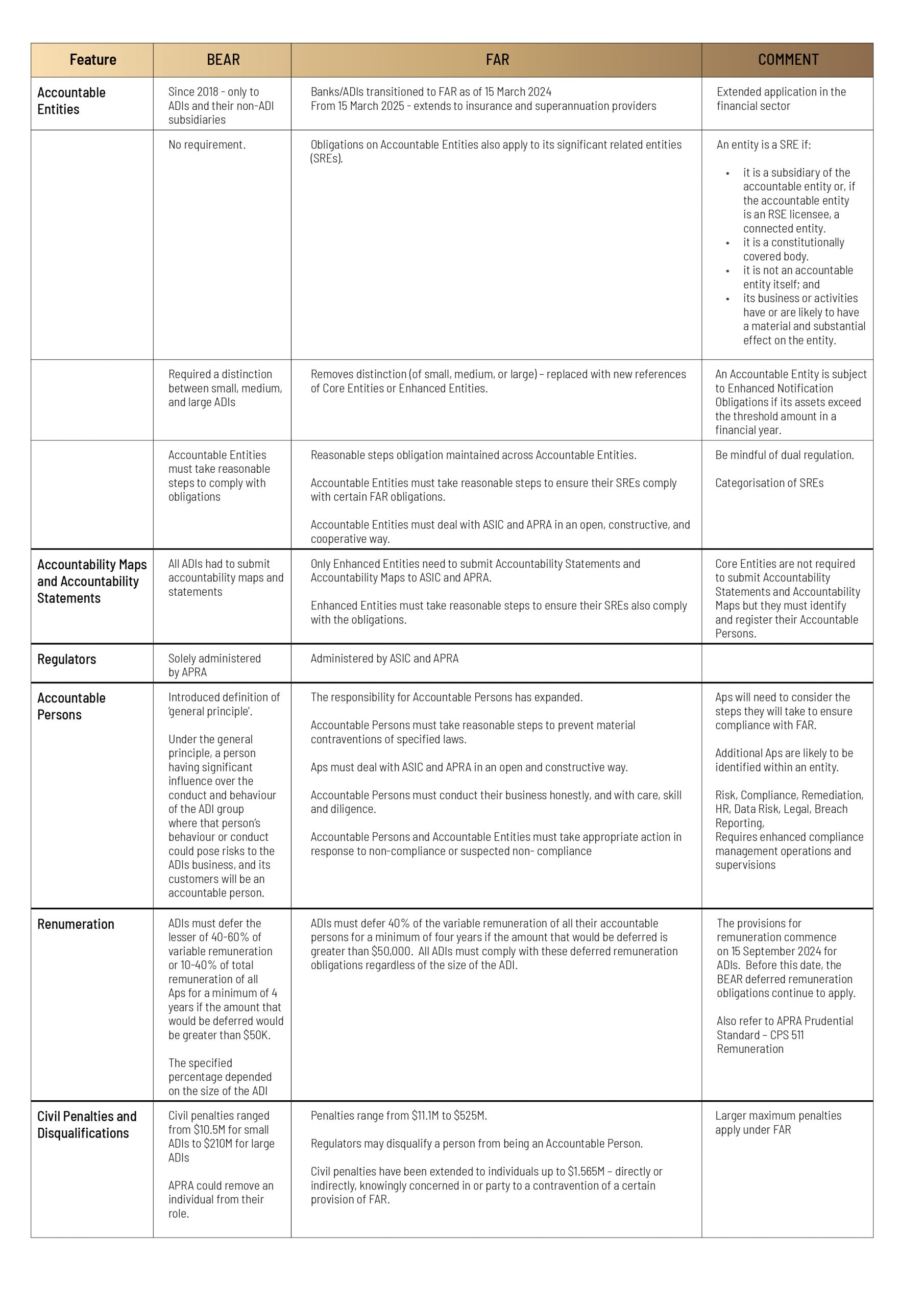

Key changes for Accountable Entities

FAR introduced several changes outlined in the table below:

Key Considerations for Accountable Entities & Accountable Persons

Accountable Entities and their nominated Accountable Persons should review their ‘lines of business’ to align with the FAR key functions and responsibilities. Accountable Entities should attend to any compliance or reporting gaps before March 2025. This should include reviewing:

- ‘Lines of business’ and the governance transparency available to the Accountable Person.

- For ADIs, determining who fulfils the role of Accountable Person for each of the new responsibilities – Breach Reporting, Remediation, and Dispute Resolution.

- For all Accountable Entities, implementing controls for the FAR responsibilities of the Accountable Entity and visibility to the Accountable Person. Documenting the processes would help demonstrate the reasonable steps being taken.

- Review corporate insurance policies and indemnities.

- Accountable Persons should refresh their training of regulatory obligations and duties under the Corporations Act with respect to their FAR obligations.

- Assess the overlap for other key personnel and required positions – e.g. responsible managers and fit and proper persons.

Enhanced Notification Obligations

In addition to the above, the FAR introduces a concept of ‘enhanced notification obligations’ that requires only enhanced entities to prepare, submit and notify APRA and ASIC of accountability statements and accountability maps, as well as material changes to these[i]. An accountability statement applies to each Accountable Person and outlines the operations under their oversight. An accountability map shows the reporting lines within the entity. Under the current Minister Rules, the enhanced notification obligation applies to an entity subject to it having total assets greater than [ii]:

- ADIs $20 billion

- General insurers $10 billion

- Life companies $10 billion

- Private health insurers $3 billion

- RSE licensees $30 billion

The enhanced notification obligations provide APRA and ASIC with visibility into the lines of accountability governance within the ADI.

Next steps

Madison Marcus has subject matter expertise in FAR and may customise and deliver FAR training for your accountable business. Alternatively, by registering your details using the following link, please register for our next training program for ‘Accountable Persons: Implications for Directors and Officers‘, which will be held in person at our Sydney office.

We look forward to seeing you.

[i] Paragraph 1.7 of the Revised Explanatory Memorandum for the Treasury Laws Amendment (Banking Executive Accountability and Related Measures) Bill 2017 [ii] Section 9 of the Financial Accountability Regime Act 2023 (Cth) (FAR Act) [iii] Section 10 of the FAR Act. [iv] Section 21 of the FAR Act. [v] Notification under FAR remains through APRA Connect. [vi]Section 14 of Financial Accountability Regime (Minister) Rules 2024.